The 2023 Federal Tax Brackets

The Federal Income Tax Brackets for 2023 have been released. These brackets are adjusted each year to account for inflation. Therefore, if you are interested in these changes and the impact of above-average inflation in 2022 then you have come to the right place!

Key Takeaways:

· What are Income Tax Brackets?

· The Federal Tax Brackets in 2023

· The CT State Income Tax in 2022

· Strategies to Reduce Your Taxable Income

· Other Changes in 2023

What are Income Tax Brackets?

Income tax brackets are created by the Internal Revenue Service (IRS) to show citizens how much tax they will pay on each segment of their taxable income. These brackets are often described as buckets because once the first bucket is filled it flows to the next and so on. The first income tax bracket is 10%, which then flows to the 12%, 22%, 24%, 32%, 35%, and lastly the 37% tax bracket in that order. For this reason, retirees often pay a maximum tax rate of 24% due to their reduced income in retirement.

The Federal income taxes in the United States are progressive so the higher the taxable income, the higher the percentage of taxes to be paid on it. For example, an individual with $300,000 of taxable income will pay a larger percentage of tax on their income compared to an individual with $60,000 of taxable income. The single filer with $60,000 of taxable income would fill the 10% and 12% buckets, with the remaining amount of income subject to 22% tax for an average income tax rate of 14%. Compared to the person with $300,000 of taxable income who would fill more buckets and consequently pay an average income tax rate of over 25%.

The Federal Tax Brackets in 2023

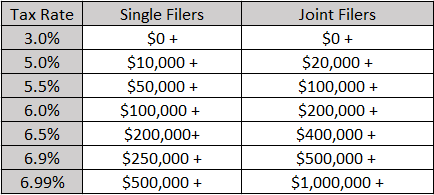

The CT State Tax Brackets in 2022

*We are still waiting on the release of the 2023 CT State Income Tax rates

Strategies to Reduce Your Taxes

There are several strategies to lower your taxable income, but I will focus on three. The first strategy is to contribute to a tax-deferred retirement account such as a 401(k) or Traditional IRA. The 2023 contribution limit for a 401(k) is $22,500 while the limit for a Traditional IRA is $6,500 and $7,500 for individuals aged 50 and older. You can deduct the contributions you make to these accounts from your taxable income because the taxes are paid when the money is withdrawn.

The next strategy is to contribute to a Health Savings Account (HSA). An HSA is a useful account because you can contribute pre-tax money where the money can be invested. Those investments can then grow tax-free and be withdrawn tax-free for qualified medical expenses. You may hear it referred to as a “triple tax advantage” account for this reason. The one issue with an HSA is that it’s only available to individuals on a high-deductible health plan. For more information, listen to my podcast How to Make the Most of your Health Savings Account.

The final strategy is to take advantage of tax-loss harvesting. This can only be used in your taxable investment accounts. The strategy involves selling your positions at a loss to offset your capital gains. This strategy is typically used to reduce short-term gains but can also be used for long-term gains. You can deduct up to $3,000 of net losses from your taxable income. However, you cannot deduct more than your total capital losses for the year. While any losses above the $3,000 limit are carried forward.

Other Changes in 2023

There are a few other changes set for 2023 that are worth your attention. The individual standard deduction has increased to $13,850 while the deduction for married couples filing jointly increased to $27,700. The 2023 standard deduction increased by $900 for individuals and $1,800 for couples filing jointly. While the Alternative Minimum Tax exemption amount increased to $81,300 for individuals and $126,500 for married couples filing jointly.

Additionally, the maximum income tax credit amount for qualifying taxpayers with three or more children increased to $7,430. This amount increased from $6,935 in 2022 which was likely caused by the increased cost of living due to inflation. The maximum credit for adoptions increased significantly as well, up to $15,950 in 2023. Lastly, the annual gift exclusion increased by $1,000 to $17,000 in 2023.